Key Takeaways

- Strong Start to the Year Confirms Outlook: Despite the decline in rare earth prices, with $10.8 million of Adjusted EBITDA(1), Neo is off to a strong start to fiscal year 2024 and is on path to meet its outlook for double-digit percentage growth in Adjusted EBITDA(I) for fiscal year 2024, as compared to fiscal year 2023.

- Strong Cash and Liquidity Position: Neo’s maintains a strong cash position as at March 31, 2024 with $101.7 million of cash and $170.6 million of inventory.

- Rare Metals Performance Bounces Back Quarter Over Quarter and Confirming Outlook: The Rare Metals business unit bounced back from Q4 2023 results with Adjusted EBITDA(I) on path to exceed 2023 Full Year results.

- Silmet Rare Metals Operational Transformation Bearing Fruit: The closure of the midstream hydromet process for tantalum and niobium at Silmet, completed in Q4 2023, shows initial positive results as transformation continues with shift to operational improvements and opportunities for higher value sales. Neo expects to reduce inventories by the end of the year.

- Closure of Separation Operations at Zibo: In Zibo, China, Neo closed the light rare earth separation operation in April 2024. This closure is expected to improve Return on Capital Employed (“ROCE“), reduce earnings volatility and decrease the concentration risk in China. The closure is not expected to have a negative impact on Adjusted EBITDA(1) going forward, and is expected to benefit overall cash.

- Rare Earth Separation Gross Margins Negative but Significant Positive Margins in Downstream: The rare earth separation business continued to be adversely affected by the declining rare earth price environment. The downstream segments of Neo report strong positive margins where Neo’s margin are driven by high value-add operations.

- Major De-Risking of NAMCO Plant Construction — Almost Complete & Under Budget: Neo’s new relocated and modernized manufacturing plant for specialty materials for automotive emissions control catalysts is now almost complete. Continuing customer qualifications and expecting to be running full production again by the end of the year. Expected to be completed $5.0 million under budget.

- Europe Sintered Magnet Plant Construction — On Time & On Budget: Neo is about halfway into the construction and the project continues to be within the original budget.

- Additional Outside-of-China Feedstock Partnerships: Neo executed a Memorandum of Understanding (“MOU“) with Meteoric Resources for rare earth supply to Neo’s European midstream facility and to support Neo’s sintered magnet facility in Europe.

Q1 2024 Highlights

(unless otherwise noted, all financial amounts in this news release are expressed in United States dollars)

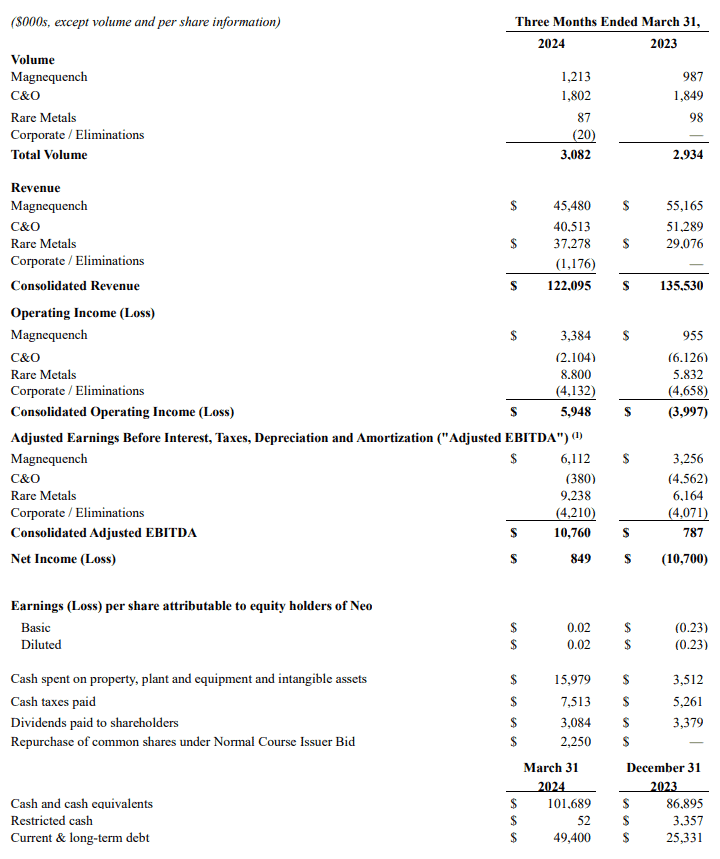

- Neo’s Q1 2024 revenue was $122.1 million, vs Q4 2023 revenue of $128.7 million; vs Q1 2023 revenue of $135.5 million.

- Operating income for Q1 2024 was $5.9 million, vs Q4 2023 operating loss of $5.5 million; vs Q1 2023 operating loss of $4.0 million.

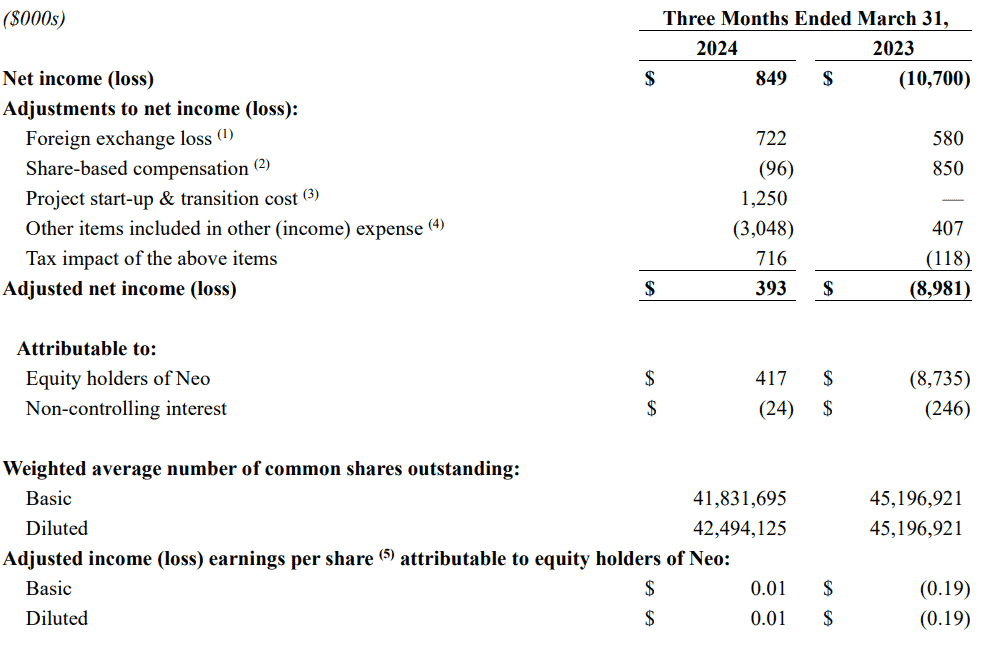

- Adjusted Net Income(1) for Q1 2024 was $0.4 million, or $0.01 per share, vs Q4 2023 of $0.9 million or $0.02 per share; vs Q1 2023 Adjusted Net Loss of $9.0 million or $0.19 per share.

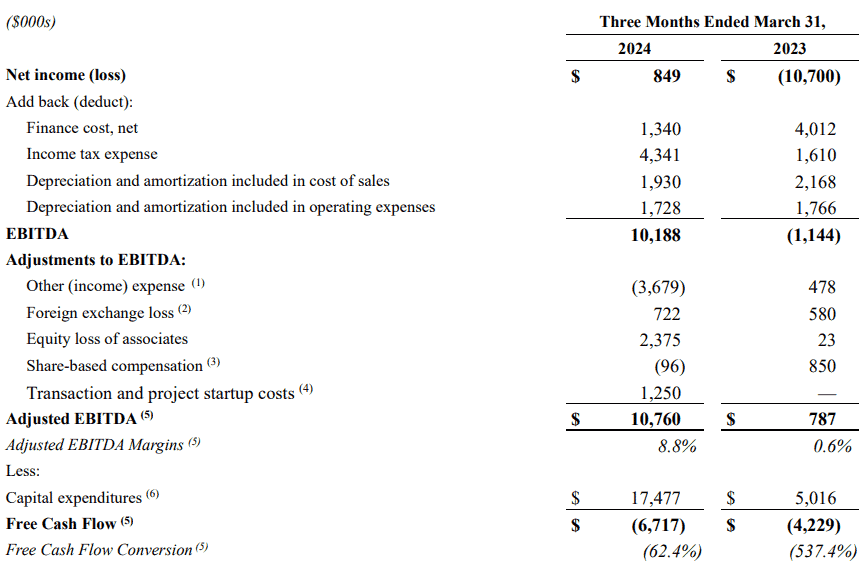

- Adjusted EBITDA(1) for Q1 2024 was $10.8 million, vs Q4 2023 of $3.1 million; vs Q1 2023 of $0.8 million.

- Neo’s cash balance was $101.7 million, after spending $16.0 million on capital projects, distributing $3.1 million in dividends to Neo’s shareholders, and repurchasing $2.3 million of common shares under the normal course issuer bid.

- A quarterly dividend of Cdn$0.10 per common share was declared on May 8, 2024 for shareholders of record on June 18, 2024, with a payment date of June 27, 2024.

“Neo began the year in a strong position, considering the underlying pricing environment,” said Rahim Suleman, President and CEO. “Despite continued pressure on rare earth prices and softer magnetic demand which contributed to lower revenue, we generated improved gross profit and improved Adjusted EBITDA(1) on both a sequential and year over year basis. We benefited from another strong quarter of our Rare Metals business unit and are encouraged by the supportive results in Magnequench and automotive catalysts. Overall, the first quarter is aligned with our outlook of double-digit Adjusted EBITDA(1) growth for 2024.”

On strategic initiatives, Rahim Suleman added “The future of our Company continues to be shaped by the strategic review of all of our operating assets and strategies and our team’s execution of our plan to achieve higher ROCE and reduce earnings volatility across each of our businesses. During the first quarter, (i) we began commissioning our newly constructed environmental catalyst plant, (ii) we changed the operational footprint in Zibo (China) by shutting down light rare earth separation lines, (iii) we began to see the fruits of our Silmet Rare Metals transformation plan announced in Q4 2023, (iv) we continued to build our new sintered magnet facility in Europe, and (v) we signed an MOU with Meteoric Resources for offtake of feedstock for the new magnet facility from a mining exploration project in Brazil.”

HIGHLIGHTS OF FIRST QUARTER 2024 CONSOLIDATED PERFORMANCE

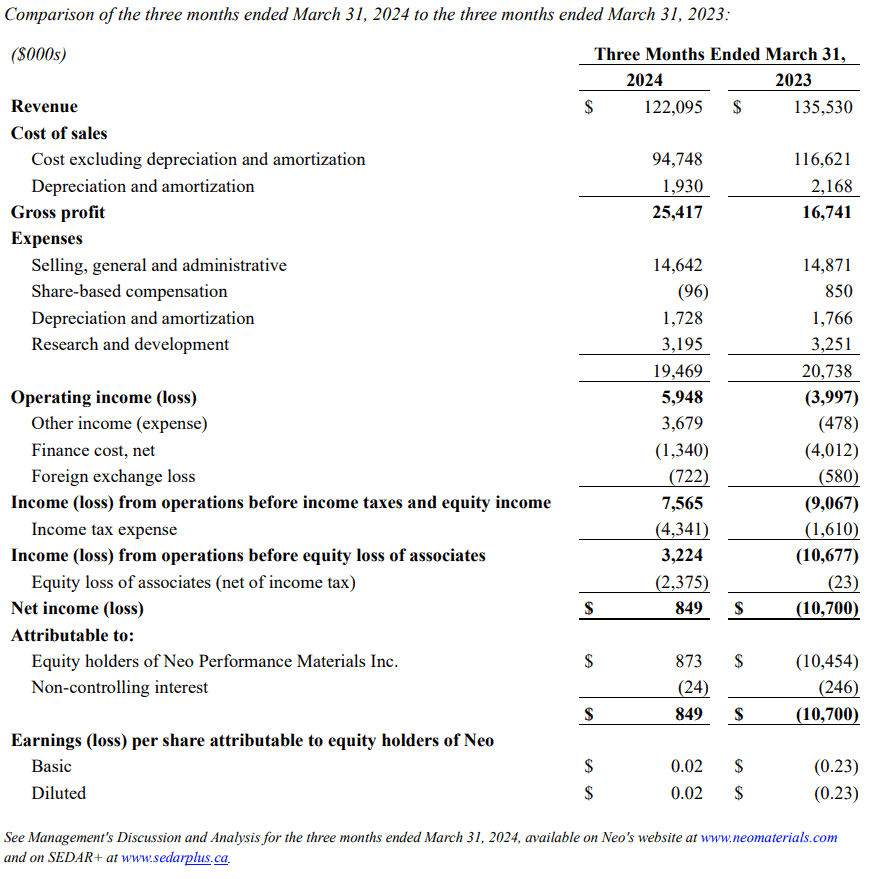

Neo’s consolidated revenue for the three months ended March 31, 2024 was $122.1 million compared to $135.5 million for the same period in the prior year. Neo reported a net income of $0.8 million, or $0.02 per share, compared to net loss of $10.7 million, or $0.23 per share, for the same period in the prior year. Adjusted Net Income(1) totaled $0.4 million, or $0.01 per share, compared to Adjusted Net Loss(1) of $9.0 million or $0.19 per share, for the same period in the prior year. Adjusted EBITDA(1) was $10.8 million, compared to Adjusted EBITDA(1) of $0.8 million for the same period in the prior year.

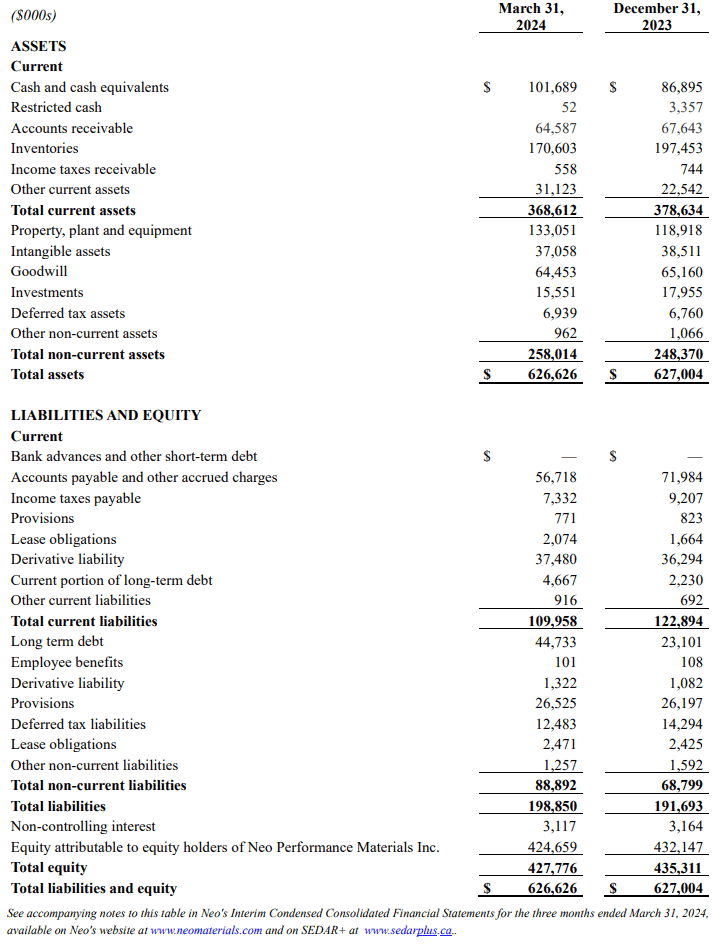

As of March 31, 2024, Neo had cash and cash equivalents of $101.7 million plus $0.1 million of restricted cash, compared to $86.9 million plus $3.4 million as at December 31, 2023.

MAGNEQUENCH

Magnequench revenue in the three months ended March 31, 2024 declined by 17.6% as compared to the prior period. Magnequench segment volumes increased by 22.9% compared to the same period in 2023, driven by growth in the magnet business and a recovery in traction motor volumes. The magnet business has been a strategic focus area for Magnequench with volume gains driven by growth in automotive applications. Magnetic heavy-rare-earth-free powders in traction motor applications also delivered substantial growth with first quarter volume up more than 300% compared to the same period in 2023, as the market recovers back to run rate levels with additional upside driven by customer inventory build ahead of new vehicle model launch. Although the business had a strong quarter, volumes remain below expectations as demand remains soft within the remaining portion of the magnetic powder business. As majority of Magnequench contracts have pass-through rare earth pricing, relative to the other business units, declining rare earth prices put relatively less pressure on Magnequench gross margin, which is close to management’s expectations. On operational improvements, Magnequench continued building on its progress in reducing conversion costs by 20% last year.

CHEMICALS & OXIDES ("C&O")

For the three months ended March 31, 2024, C&O revenue declined by 21.0% as compared to prior period, primarily due to rare earth pricing headwinds. The impact of declining market prices drove negative gross margins within the rare earth separation portion of the business. The C&O business faced challenges from falling rare earth prices, leading to unfavourable lead-lag effects as materials bought at higher costs three to five months earlier were processed. Additionally, the demand for high value rare earth elements has been slower than historical levels. The environmental emissions catalyst business saw volumes and margins at the lower end of the expected levels range, primarily as a result of shipping delays and delivery timelines. The environmental protective water treatment solutions business achieved its fifth consecutive quarter of volume growth and record gross margins.

RARE METALS

Rare Metals revenue improved by 28.2% in the three months ended March 31, 2024, as compared to the same period in 2023. In the first quarter of 2024, results returned to 2022 and 2023 levels with resetting of prices and spot demand. The segment has a healthy hafnium order book for 2024 with contracted volumes at strong pricing and sufficient inventory on hand. Rare Metals is beginning to see early positive results from the change it made in its manufacturing strategy with its Silmet plant, shifting focus on downstream, value-add operations, by halting the energy-intensive hydrometallurgical processing of niobium and tantalum bearing ores. Going forward, future products will be derived from oxides and recycled materials which will increase sourcing optionality and reduce working capital, simplify the manufacturing process, and improve the environmental footprint of the plant. The focus now is on improving historical yields and efficiency in the higher value finishing processes

Q1 2024 UPDATE ON STRATEGIC INITIATIVES

NAMCO Relocation, Upgrade and Modernization

Project nearing completion with $5.0 million under-spend to budget anticipated

Neo has almost completed the relocation, upgrade and modernization of its environmental emissions catalyst manufacturing facility to a newly built site in an industrial park, equipped with advanced infrastructure, transportation, and wastewater treatment capabilities. The nearly completed facility began quality assurance testing for customer samples in the first quarter and, pending customer approval, is expected to achieve full production by the second half of 2024. Neo’s initial budget for the expansion, upgrade, and relocation of the facility was $75.0 million. With the project nearing completion, and purchase orders issued for over 90% of projected project spend, the current estimated spend is approximately $70.0 million ($5.0 million below budget). Neo spent $8.6 million on the project during the first quarter of 2024 and $42.2 million since commencement of the relocation efforts. The majority of the remaining cost to complete of $27.8 million is expected to be spent in 2024. To fund these efforts, Neo secured a $75.0 million credit facility from Export Development Canada (“EDC“) in August 2022, drawing $50.0 million by March 2024 to cover these costs.

Sintered Magnet Plant in Europe

Project continues to be on time and on budget

Neo is advancing a manufacturing facility in Europe to produce sintered magnets essential for applications like electric vehicle traction motors and wind turbine generators. This helps European OEMs fulfill the domestic sourcing targets set by the European Union (“EU“) Critical Raw Materials Act. The initial phase of the project, based in Narva, Estonia, near Neo’s Silmet facility, aims to produce 2,000 tonnes per year of magnet capacity, with plans to increase to 5,000 tonnes and potential subsequent expansion into North America. The strategy encompasses supply security, manufacturing competence, market competitiveness, customer engagements, and financing, including both company and government funds. On November 9, 2022, Neo received a grant of up to $20.2 million from Estonia’s Just Transition Fund (“JTF“) for this project, marking a significant EU endorsement. The project, expected to cost approximately $75.0 million for Phase 1, is on track and on budget, with $15.0 million already spent ($6.0 million of which in Q1 2024) and an estimated $60.0 million to be invested through 2024 into 2025 (prior to the JTF grant).

Impact of Rare Earth Prices on Separation Gross Margins

In the first quarter of 2024, rare earth prices continued to decrease, with neodymium and praseodymium prices falling by about 20% and dysprosium and terbium prices by around 30%. These sharp declines adversely affected profit margins, primarily in the C&O rare earth separation business which delivered a gross margin loss of $3.0 million in the first quarter of 2024. Neo is focused on reducing this earnings volatility through commercial and operational action; as well as portfolio actions which include the recent announced closure of light rare earth separation in Zibo, China. By winding down Zibo’s midstream rare earth operations, Neo will free up working capital to further pursue growth in higher return, value-add downstream businesses.

Operational Footprint Change in Zibo, China

Delivery of manufacturing transformations to improve ROCE and reduce earnings volatility

Neo ceased production of its light rare earth separations in Zibo, China. Neo will continue to manufacture value-add specialty products at its new environmental emissions catalyst facility (NAMCO), also located in Zibo, China. Management expects minimal cash costs associated with this action in Zibo, as Neo intends to temporarily transfer affected employees to the new specialty products facility (NAMCO) and has entered into negotiations with third parties regarding the continued employment of such ZAMR employees in the longer term. All remaining inventory is expected to either be sold or absorbed into the remaining Neo business. Neo anticipates taking a non-cash charge to its second quarter net income/(loss) of less than $2.0 million for impairment of assets as most of the capital assets have been fully depreciated. This operating footprint change is in line with Neo’s continuous improvement strategy to: (i) improve return on capital employed, as ZAMR produced low returns relative to the capital tied up; (ii) reduce overall Company earnings volatility; (iii) evaluate assets in commoditized and operationally constrained business environments. Neo continues to separate midstream rare earth oxides at other facilities located in China and Europe.

Sourcing and Rare Earth Supply Strategy

Neo is recognized globally for its diverse rare earth value-add operations, with separation and manufacturing facilities both inside and outside of China. Neo also maintains a global network of recycled scrap metal suppliers, aligning its sourcing strategies to meet the varied demands of its international customers. The C&O business unit has the most diverse global sourcing feedstock strategy, procuring rare earth materials from at least four countries, to ensure a consistent and widespread supply to support its separation and value-add activities. In addition to three previously announced MOUs for additional global sourcing, a notable and recent development includes:

- On May 1, 2024, Neo and Meteoric Resources (“Meteoric“) entered into a non-binding MOU for offtake of 3,000 tonnes rare earth oxide per year from Meteoric’s Caldeira Project in Minas Gerais, Brazil, to supply Neo’s sintered magnet manufacturing plant in Europe. This annual offtake could supply Neo with as much as 900 MT of Nd-Pr oxide and 30 MT of Dy-Tb oxide, combined, to supply Neo’s sintered magnet plant in Europe, currently under construction.

CASH ALLOCATION HIGHLIGHTS

- As at March 31, 2024, Neo had $101.7 million in cash, $0.1 million in restricted cash, offset by $49.4 million drawn from its EDC facility credit facility, resulting in net cash of $52.3 million. Neo repaid $1.5 million of term loan facilities at SG Technologies Group Limited and its wholly-owned subsidiaries (collectively referred to as “SGTec“) in the three months ended March 31, 2024.

- Cash from operating activities was $11.3 million for the three months ended March 31, 2024. Cash generation was driven by working capital performance, specifically, reductions of inventory as Neo continued to convert its higher-cost rare earth feedstock; as well as release of strategic inventory held to support contracted hafnium volumes in the first quarter of 2024.

- Neo invested $16.0 million in capital expenditures for the three months ended March 31, 2024, compared to $3.5 million for the three months ended March 31, 2023. Of this amount, $8.6 million was related to NAMCO relocation, upgrade and modernization, $1.1 million of borrowing costs related to the EDC credit facility, and $6.0 million for the establishment of the sintered magnet manufacturing plant in Europe.

- Neo has shown strong commitment to returning capital to shareholders. For the three months ended March 31, 2024, Neo repurchased and cancelled 398,871 shares for $2.3 million, completing the normal course issuer bid program which began in June 2023. In addition, Neo paid dividends to its shareholders of $3.1 million for the three months ended March 31, 2024.

2024 OUTLOOK

- With the first quarter consolidated Adjusted EBITDA(I) of $10.8 million, Neo had a strong start to the year, despite declining rare earth prices in the first quarter.

- Neo maintains an outlook for double-digit percentage Adjusted EBITDA(I) growth for fiscal year 2024 as compared to fiscal year 2023.

CONFERENCE CALL ON FRIDAY MAY 10, 2024 AT 10 AM EASTERN

Management will host a teleconference call on Friday, May 10, 2024 at 10:00 a.m. (Eastern Time) to discuss the first quarter 2024 results. Interested parties may access the teleconference by calling (416) 764-8650 (local) or (888) 664-6383 (toll free long distance) or by visiting https://app.webinar.net/EQKDyNwYkBj. A recording of the teleconference may be accessed by calling (416) 764-8677 (local) or (888) 390-0541 (toll free long distance), and entering pass code 791275# until June 10, 2024.

NON-IFRS MEASURES

This news release refers to certain non-IFRS financial measures and ratios such as “Adjusted Net Income”, “EBITDA”, “Adjusted EBITDA”, and “Adjusted EBITDA Margin”. These measures and ratios are not recognized measures under IFRS, do not have a standardized meaning prescribed by IFRS, and may not be comparable to similar measures presented by other companies. Rather, these measures and ratios are provided as additional information to complement IFRS financial measures by providing further understanding of Neo’s results of operations from management’s perspective. Neo’s definitions of non-IFRS measures used in this news release may not be the same as the definitions for such measures used by other companies in their reporting. Non-IFRS measures and ratios have limitations as analytical tools and should not be considered in isolation nor as a substitute for analysis of Neo’s financial information reported under IFRS. Neo uses non-IFRS financial measures and ratios to provide investors with supplemental measures of its base-line operating performance and to eliminate items that have less bearing on operating performance or operating conditions and thus highlight trends in its core business that may not otherwise be apparent when relying solely on IFRS financial measures. Neo believes that securities analysts, investors and other interested parties frequently use non-IFRS financial measures and ratios in the evaluation of issuers. Neo’s management also uses non-IFRS financial measures to facilitate operating performance comparisons from period to period. For definitions of how Neo defines such financial measures and ratios, please see the “Non-IFRS Financial Measures” section of Neo’s management’s discussion and analysis filing for the three months ended March 31, 2024, available on Neo’s web site at www.neomaterials.com and on SEDAR+ at www.sedarplus.ca.

TABLE 5: CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

TABLE 6: CONSOLIDATED RESULTS OF OPERATIONS

TABLE 7: RECONCILIATIONS OF NET INCOME (LOSS) TO EBITDA, ADJUSTED EBITDA AND FREE CASH FLOW

Notes:

- Represents other (income) expenses resulting from non-operational related activities, including provisions for damages for outstanding legal claims related to historic volumes. In addition, other income for the three months ended March 31, 2024 includes a reversal of special reserve to cover potential liabilities related to employee safety incidents or workplace accidents at C&O’s Zibo Jiahua Advanced Material Resources Co., Ltd. (“ZAMR”) facility in China. This reserve was set up since inception of the light rare earth separation business and has been released as Neo has winded down operations. These income and expense are not indicative of Neo’s ongoing activities.

- Represents unrealized and realized foreign exchange losses that include non-cash adjustments in translating foreign denominated monetary assets and liabilities.

- Represents share-based compensation expense in respect of the Omnibus LTIP and the LTIP.

- These represent primarily legal, professional advisory fees and other transaction costs related to sintered magnet start-up cost, as well as transition cost during qualification start-up of NAMCO facility and the winding down of ZAMR. Neo has removed these charges to provide comparability with historic periods.

- Neo reports non-IFRS measures such as “Adjusted Net Income”, “Adjusted Earnings per Share”, “Adjusted EBITDA”, “Adjusted EBITDA Margin”, “Free Cash Flow” and “Free Cash Flow Conversion”. Please see information on this and other non-IFRS measures in the “Non-IFRS Measures” section of this news release and in the MD&A, available on Neo’s website neomaterials.com and on SEDAR+ at www.sedarplus.ca.

- Includes cash and non-cash capital expenditures of $16.6 million and right-of-use assets of $0.9 million for the three months ended March 31, 2024. For the three months ended March 31, 2023, the amount was comprised of capital expenditures of $3.5 million and right-of-use assets of $1.5 million

TABLE 8: RECONCILIATIONS OF NET INCOME (LOSS) TO ADJUSTED NET (LOSS) INCOME

- Represents unrealized and realized foreign exchange losses that include non-cash adjustments in translating foreign denominated monetary assets and liabilities.

- Represents share-based compensation expense in respect of the Omnibus LTIP and the LTIP.

- These represent primarily legal, professional advisory fees and other transaction costs related to sintered magnet start-up cost, as well as transition cost during qualification start-up of NAMCO facility and the winding down of ZAMR. Neo has removed these charges to provide comparability with historic periods.

- Represents other (income) expenses resulting from non-operational related activities, including provisions for damages for outstanding legal claims related to historic volumes. In addition, other income for the three months ended March 31, 2024 includes a reversal of special reserve to cover potential liabilities related to employee safety incidents or workplace accidents at C&O’s ZAMR facility in China. This reserve was set up since inception of the light rare earth separation business and has been released as Neo has winded down operations. These income and expense are not indicative of Neo’s ongoing activities.

- Neo reports non-IFRS measures such as “Adjusted Net Income”, “Adjusted Earnings per Share”, “Adjusted EBITDA”, “Adjusted EBITDA Margin”, “Free Cash Flow” and “Free Cash Flow Conversion”. Please see information on this and other non-IFRS measures in the “Non-IFRS Measures” section of this news release and in the MD&A, available on Neo’s website neomaterials.com and on SEDAR+ at www.sedarplus.ca.

Information Contacts

Ali Mahdavi

SVP, Corporate Development & Capital Markets

(416) 962-3300

Email: a.mahdavi@neomaterials.com

George Gretes

Communications & Media

(647) 294-7244

Email: media@neomaterials.com

Cautionary Statements Regarding Forward Looking Statements

This news release contains “forward-looking information” within the meaning of applicable securities laws in Canada. Forward-looking information may relate to future events or the future performance of Neo. All statements in this release, other than statements of historical facts, with respect to Neo’s objectives and goals, as well as statements with respect to its beliefs, plans, objectives, expectations, anticipations, estimates, and intentions, are forward-looking information. Specific forward-looking statements in this discussion include, but are not limited to, the following: expectations regarding certain of Neo’s future results and information, including, among other things, revenue, expenses, sales growth, capital expenditures, and operations; statements with respect to current and future market trends that may directly or indirectly impact sales and revenue of Neo; expected use of cash balances; continuation of prudent management of working capital; source of funds for ongoing business requirements and capital investments; expectations regarding sufficiency of the allowance for uncollectible accounts and inventory provisions; analysis regarding sensitivity of the business to changes in exchange rates; impact of recently adopted accounting pronouncements; risk factors relating to intellectual property protection and intellectual property litigation; risk factors relating to national or international economies, geopolitical risk and other risks present in the jurisdictions in which Neo, its customers, its suppliers, and/or its logistics partners operate, and; expectations concerning any remediation efforts to Neo’s design of its internal controls over financial reporting and disclosure controls and procedures. Often, but not always, forward-looking information can be identified by the use of words such as “plans”, “expects”, “is expected”, “budget”, “scheduled”, “estimates”, “continues”, “forecasts”, “projects”, “predicts”, “intends”, “anticipates” or “believes”, or variations of, or the negatives of, such words and phrases, or state that certain actions, events or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved. This information involves known and unknown risks, uncertainties and other factors that may cause actual results or events to differ materially from those anticipated in such forward-looking information. Neo believes the expectations reflected in such forward-looking information are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward-looking information included in this discussion and analysis should not be unduly relied upon. For more information on Neo, investors should review Neo’s continuous disclosure filings that are available under Neo’s profile at www.sedarplus.ca.